The HUD 4001.1 HANDBOOK clearly states debt to income ratio requirements for FHA manual underwriting mortgages. … 580 and above – max DTI is 31% / 43% WITHOUT compensating factors. 580 and above – max DTI is 37% / 47% with ONE compensating factor. 580 and above – max DTI is 40% / 50% with at least TWO compensating …

What is the FHA manually underwritten housing ratio?

To recap, FHA’s maximum qualifying debt ratios for borrowers in 2021 are 31% and 43%. This means the monthly housing payments should not exceed 31% of gross monthly income, while the total debt burden should not exceed 43% of monthly income. But there are exceptions to these rules, as noted above.

Does FHA allow manual underwriting?

Only FHA and VA loans allow for manual underwriting. Conventional loans cannot be manually underwritten. The mortgage underwriter has a lot of underwriter discretion on manual underwriting files. The key in getting approved on manual underwrites is timely payments in the past 24 months.

What are FHA qualifying ratios?

With the FHA, you’re generally required to have a DTI of 43% or less, though it varies based on credit score. To be more specific, your front-end DTI (monthly mortgage payments only) should be 31% or less, and your back-end DTI (all monthly debt payments) should be 43% or less.What is a manual underwrite for FHA loan?

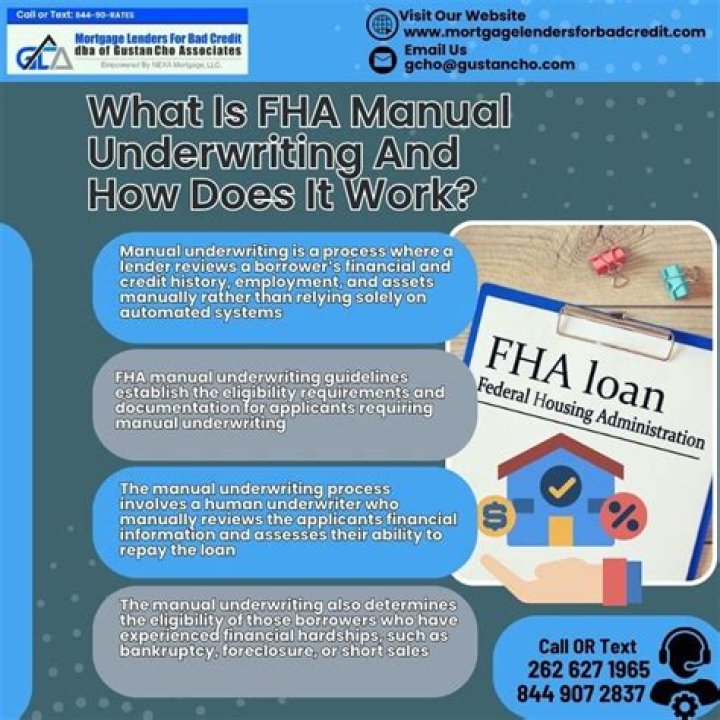

During manual underwriting, an actual underwriter analyzes your finances and decides whether you qualify for a mortgage. Manual underwriting requires more paperwork than automated underwriting, and it also takes more time. Your underwriter will ask for documents like tax returns and bank statements.

What are red flags for underwriters?

Red–flag issues for mortgage underwriters include: Bounced checks or NSFs (Non–Sufficient Funds charges) Large deposits without a clearly documented source. Monthly payments to an individual or non–disclosed credit account.

Can I get a mortgage with 55% DTI?

FHA loans only require a 3.5% down payment. High DTI. If you have a high debt-to-income (DTI) ratio, FHA provides more flexibility and typically lets you go up to a 55% ratio (meaning your debts as a percentage of your income can be as much as 55%). Low credit score.

How is housing ratio calculated?

To calculate the housing expense ratio, simply take the sum of all property expenses and divide it by a pretax income.What are the FHA loan limits for 2020?

Thanks to increases in home prices in 2019, the Federal Housing Administration loan limit will increase for nearly all of the country in 2020. According to an announcement from the FHA, the 2020 FHA loan limit for most of the country will be $331,760, an increase of nearly $17,000 over 2019’s loan limit of $314,827.

What does housing ratio mean?The housing expense ratio, also called the front-end ratio, is a percentage determined by dividing the borrower’s housing expenses by their pre-tax income. At its most basic, it’s a simple number showing how much of your income goes to paying for housing, and considers your mortgage payment, insurance, taxes and more.

Article first time published onHow long does manual FHA underwriting take?

When you apply for this type of mortgage, the underwriter will make sure that your application meets both the lender’s standards as well as the standards set forth by the FHA. FHA loans take an average of 55 days to close. For home purchases, the average is 54 days. For refinances, it’s 59 days.

What is an FHA manual downgrade?

Manual underwriting is when a borrower cannot get an approve/eligible per automated underwriting system (AUS). … Borrowers who get a refer/eligible per automated underwriting system are eligible for manual underwriting on FHA and VA loans.

How long does automated underwriting take?

Automated underwriting makes the first phase of the underwriting process much more efficient. It has the capability to provide instant outputs that can generally take up to 60 days to complete with manual processing.

Who uses manual underwriting?

Some types of mortgages require manual underwriting if the borrower doesn’t meet certain standards. For instance, FHA loans require manual underwriting when a borrower has a credit score of 620 or below and a debt-to-income ratio of 43 percent or more.

Is FHA underwriting automated?

FHA TOTAL is accessed through an automated underwriting system, and it ensures that FHA loan applicants are evaluated by the same scoring process and enhances FHA’s ability to assess and manage risk.

Can underwriters make exceptions?

There are typically two types of loan exceptions: 1) Policy exceptions and 2) underwriting exceptions. … When a borrowers credit score, debt-to-income ratio, or loan-to-value ratio do not meet the organization’s defined standards, an underwriting exception occurs.

What is the maximum DTI for FHA?

FHA Loans. FHA loans are mortgages backed by the U.S. Federal Housing Administration. FHA loans have more lenient credit score requirements. The maximum DTI for FHA loans is 57%, although it’s lower in some cases.

What is the max debt-to-income ratio for a conventional loan?

Conventional loans (backed by Fannie Mae and Freddie Mac): Max DTI of 45% to 50%

How can I lower my debt-to-income ratio for a mortgage?

- Lower the interest on some of your debts. …

- Extend the duration of your loans …

- Find a source of side income. …

- Look into loan forgiveness. …

- Pay off high interest debt. …

- Lower your monthly payment on a debt. …

- Control your non-essential spending.

Is no news good news with underwriting?

When it comes to mortgage lending, no news isn’t necessarily good news. … Particularly in today’s economic climate, many lenders are struggling to meet closing deadlines, but don’t readily offer up that information.

Why would an underwriter deny an FHA loan?

There are three popular reasons you have been denied for an FHA loan–bad credit, high debt-to-income ratio, and overall insufficient money to cover the down payment and closing costs.

What is the final review in underwriting?

Loan funding: The “final” final approval This means the lender has reviewed your signed documents, re–pulled your credit, and made sure nothing changed since the underwriter’s last review of your loan file. When the loan funds, you can get the keys and enjoy your new home.

What is the maximum 203k loan amount?

What is the maximum 203k loan amount? You can borrow up to 110 percent of the property’s proposed future value, or the home price plus repair costs, whichever is less.

Are FHA loan limits increase in 2022?

FHA loan limits are increasing in 2022. The new baseline limit – which applies to most single–family homes – will be $420,680. That’s nearly a $65,000 increase over last year’s FHA loan limit of $356,360. The Federal Housing Administration is raising its lending limits to keep pace with home price inflation.

What should your housing ratio be?

The housing expense ratio is the percentage of your gross monthly income devoted to housing expenses. … Typically, this ratio should not exceed 28%. The bottom ratio is equal to your new monthly mortgage payment plus your monthly debt divided by your gross income per month. Typically, this ratio should not exceed 36%.

What percent is the normal range for a housing ratio?

Lenders generally look for the ideal front-end ratio to be no more than 28 percent, and the back-end ratio, including all monthly debts, to be no higher than 36 percent.

What are the ratios typically called in qualifying?

Lenders normally use one of two qualification ratios in their underwriting process. The first is the monthly debt-to-income ratio (DTI) while the second one is called the back-end ratio, which calculates the monthly debt payment to income.

Do FHA loans get rejected in underwriting often?

But it’s important to remember that an FHA loan could still be rejected in underwriting, even if you’ve been pre-approved already. While it doesn’t happen often, this is a realistic scenario that can affect some borrowers.

How often is a loan denied in underwriting?

One in every 10 applications to buy a new house — and a quarter of refinancing applications — get denied, according to 2018 data from the Consumer Financial Protection Bureau.

Do underwriters want to approve loans?

An underwriter will approve or reject your mortgage loan application based on your credit history, employment history, assets, debts and other factors. It’s all about whether that underwriter feels you can repay the loan that you want. … But a seasoned loan originator is the integral part of the whole process, he says.

How accurate is automated underwriting?

An automated underwriting approval is only as accurate as the information input into the system, and will only be as reliable as the documentation provided to support the information on your loan application.